401(k) plans make up a significant part of Americans’ retirement planning. According to the Investsment Company Institute, we had over $5.9 trillion in assets in 401(k) plans as of September 2019. These were being held on behalf of 55 million active participants. That’s 20% of the overall $29 trillion of retirement assets in America.

But just what is the average rate of return on a 401(k) plan in 2020? It would make sense then that many would want to see the average rate of return on 401(k) plans as high as possible.

Unfortunately, recent history reveals the average 401(k) return is below par.

Average 401(k) Return vs. The Market

Just four years ago, the average rate of return on 401(k) plans was an abysmal -.4%.

Relative to the overall return of the S&P 500 over the same time it fared a little better as the S&P had a -.7% return, however when you look at buy and hold investors they fared better at a return of 1.2%.

Looking at the recent past five years, Motley Fool found an average 401(k) return of just over 7%. While seemingly a good return, that’s compared to a near 15% return over the same timeframe for the S&P – so the average 401(k) returned less than half of the return of a broad-based index.

With that being said, what should be considered a good rate of return on your 401(k)? Christine Benz, from Morningstar, claims a return of 5% per year is a good number to use for planning.

While it’s good to have a baseline number to use for planning, 5% falls short when compared to historical returns from the S&P. Over the course of the past 20 years, the S&P 500 has returned just over 8%, according to Blackrock.

That 3% difference may not seem like much, but it can have an absolutely massive impact over the course of a career.

Why Are Average 401(k) Returns So Poor?

There are several reasons for the disparity, such as choosing (or being forced to choose) actively managed funds in your 401(k) over passively managed funds, which outperform the former.

Similarly, being fearful of the stock market may cause some investors to be overly cautious in their fund selections.

However, one of the key drivers behind the gap is the fees charged by many 401(k) plans. Those fees, when taken over the long-term can cause a serious drag on a portfolio.

For example, the SEC reports that a .75% difference in fees on a portfolio of $100,000 will cost an investor $30,000 over the course of 20 years.

Just imagine if you have a larger portfolio with a longer timeframe or a larger difference in fees. All of those factors will accelerate the erosion of your portfolio and put you further behind the overall stock market performance.

If you feel you may be paying too much in fees, using the free 401(k) fee analyzer tool at Personal Capital is a great way to find money saving options.

Do 401(k) Fees Really Affect Returns That Much?

Yes, absolutely! Because of the power of compound interest, a single 1% difference in fees can cost you hundreds of thousands of dollars over the years.

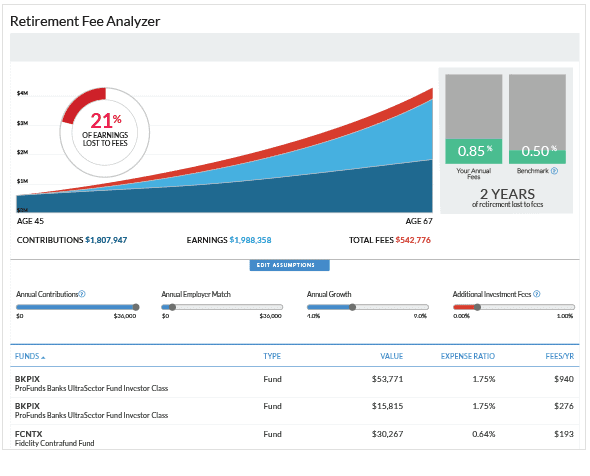

When InvestmentZen contributor Mr. 1500 ran Personal Capital’s fee analysis tool on his 401k portfolio, he nearly fell out of his chair. He discovered that with his current portfolio, he was going to pay a whopping $594,993 in fees over the next 26 years:

After he discovered this scary fact, he spent a few hours moving his investments around and reduced his potential fees to just $86,163, saving him over $500,000 dollars.

If you want to increase your 401(k) returns, signing up for a FREE account at Personal Capital to take advantage of their 401k analyzer is an easy way to do it. It might just save you $500,000 dollars (or more).

Education is Key

Fund selection and minimizing fees is certainly one key component to helping boost the average rate of return on 401(k) plans. The more diverse and low-cost options available give investors options best suited for their long-term needs. Investors can’t choose low-cost options if they’re not made available, but that covers only one way to improve 401(k) performance.

The other, equally important way to improve 401(k) performance is through education, or rather, financial literacy.

Studies show that a more financially literate individual tends to have a higher average return on his or her 401(k) plans. On a risk-adjusted basis, those who are more financially literate see a return of more than one percent per year when compared to those who are less financially literate. That adds up to a difference of 25 percent over the course of 30 years.

No study is perfect, but the cited study points out that savvier investors tend to be more comfortable with risk and thus experience a higher return in their 401(k) plans.

If you feel less than comfortable investing through your 401(k) plan, most plans offer free educational resources to equip you to make more informed investing decisions.

What About Your Old 401(k) Plans?

While 401(k) plans make up a significant amount of overall retirement planning, you shouldn’t be naïve enough to believe they’re the only tools.

You may have old 401(k) plans with former employers. You may have IRAs with online brokers you ignore. In either case, you may be paying more in fees than you realize. The average annual fee charged by a 401(k) plan is 1.29%. The average equity mutual fund charges .68%, as of 2015.

In either instance, you could be leaving money on the table if you leave a 401(k) with a former employer or ignore an IRA. There are options to help most investors slash those fees and make more of your money work for you. If you like to manage your own investments, a low-cost broker like Vanguard or Fidelity may be an option.

However, if you don’t like the idea of being a DIY investor and you’d rather have someone manage your investments for you, you can rollover a 401(k) or open an IRA with a robo-advisor like Betterment or Wealthfront, both of which will charge a fraction of the fees you currently pay to manage your portfolio of low-fee index funds.

The One Thing Guaranteed to Increase the Return on Your 401(k)

If it’s not obvious yet, the key factor in dragging down the average 401(k) return is fees. Most 401(k) plans are chock full of fees, and that does one thing – it takes money away from you and puts it in someone else’s pocket.

Unfortunately, few believe 401(k) plans actually charge fees as a recent study shows that 67 percent of individuals don’t believe there are fees in their 401(k) plan. That’s the same as thinking a car can drive without a motor.

Some of the fees that get packed into your 401(K) plans include:

- Plan administration fees

- Investment fees

- Individual services fees

The fees don’t stop there. Depending on the mutual fund you choose in your 401(k) plan you could also be paying the following fees:

- Sales charges (i.e. load funds)

- Management fees

- 12b-1 fees

- More, depending on the fund of choice

When totalled, these fees can easily equate to an additional 1-2% in charges. Those directly impact your return, to the tune of tens (if not hundreds) of thousands of dollars over your career, thanks to losses in compound interest.

In fact, that one percent difference can mean adding a decade to your retirement income.

Should we give in and assume there’s no way to cut down on these bloodsucking fees? No, there are ways to find lower fee options that will keep more money in your portfolio and, better yet, it’s not that difficult to find those cheaper alternatives.

The best tool to find those alternatives is Personal Capital. Personal Capital is a free to use service that helps you better manage your finances.

One of the best features is the fee analyzer tool. The fee analyzer tool shows you just how much your 401(k) plan, or any other investment portfolio for that matter, is costing you. It also compares your plan against other plans to get an idea of just how much in fees your plan is charging you.

It doesn’t stop there, as Personal Capital can provide lower-cost alternatives for you to consider as investment options. This may seem difficult to do, but is really as simple as a few clicks when you open a Personal Capital account as you can see in the screenshot below.

If you’ve not done so, it literally pays to check on the average rate of return of your 401(k) plan. Each money saving opportunity you find directly impacts how much your funds grow, which directly impacts how much you will have for retirement.

2 Comments